Here are some insights from the currency strategists at dailyfx. They cover the fundamentals and technicals of key Forex pairs and other key markets along with some of the key economic news of the day. Today's commentary looks at the Euro ahead of the payroll data out of the US:

Ahead of the Curve provides you with analysis and insight into today's global financial markets. The latest news and views from global stock, bond, commodity and FOREX markets are discussed.

Featured post

Time Series Analysis with GRETL

This video shows key time-series analyses techniques such as ARIMA, Granger Causality, Co-integration, and VECM performed via GRETL. Key dia...

Showing posts with label opec. Show all posts

Showing posts with label opec. Show all posts

Thursday 1 December 2016

Wednesday 30 November 2016

Daily Forex Insight

Here are some insights from the currency strategists at dailyfx.

They cover the fundamentals and technicals of key Forex pairs and other

key markets along with some of the key economic news of the day.

Today's commentary looks at whether the big market moves in November are here to stay:

Tuesday 29 November 2016

Daily Forex Insight

Here are some insights from the currency strategists at dailyfx.

They cover the fundamentals and technicals of key Forex pairs and other

key markets along with some of the key economic news of the day.

Today's commentary looks at oil and the Canadian Dollar ahead of the OPEC meeting:

Monday 21 September 2015

Five reasons why crude quotas will not support prices

Guest Post:

By:

M. S. Sriganesh

Head Sourcing

Galaxy Surfactants Limited

With sagging crude market, OPEC (Organisation of Petroleum Exporting Countries) has restarted the talk of coordinating with other producers to balance market and support prices. Though in the past quotas have worked well, this time we believe will not work. Why?

Why OPEC thinks its strategy will work:

With crude correcting more than 50% to the current levels in the proximity of $50/bbl, returns of the producers have been severely impacted. The following 5 critical data points validate the approach of OPEC to keep producing and hold market share while waiting for less efficient producers to exit:1. Crude prices in the proximity of $ 50/bbl, most producers are margin positive except for producers in US, Brazil, Russia and Canada which are the new competition. Hence at current levels for OPEC it is loss of profit rather than absolute loss while for its competitors it is an absolute loss:

2. However, over the last decade supported by high prices, producer countries have built up expenditure commitments for which a higher $/bbl price is required. Since most producers are producing at near peak capacity, increasing production to compensate is not an available option:

3. Commodity businesses are cyclical in which strong producers use up-cycles to build reserves which are used in lean periods, which is visible in this industry. Since OPEC is about National Oil Companies (NOC), Country reserves are a good measure. If the prices remain at $50/bbl levels, then except for Venezuela, Nigeria & Ecuador, most producers have a cushion to support. If the low prices continue to remain low, then the impact will spread and magnify:

4. Most producers have a high dependence on the ONG (Oil & Gas) industry with more than 30% share of the GDP:

5. Additionally, exports of these countries have a much higher skew in favor of ONG based products:

Consequentially OPEC has no option but to continue to produce to full capacity and let price fall making its more expensive competitors to exit. Quotas can be used to further reduce fragmentation in the market like in the past and get price support.

We see the above analysis optically correct while fundamentals show a different story. Here's the other picture.

5 reasons why quotas will not work:

The reason why we see this time as different is for the reasons below:1. Changed strength of OPEC:

In the 1970's OPEC has controlling more than 50% of the global production which currently has fallen to near 40%. The global consumption growth over the decades has been largely absorbed by non-OPEC production. As a result, the strength of OPEC no longer remains similar to the past with higher number of players and more fragmentation.2. Changing Customer profile:

In the 1970's, the largest consumer USA's imports were 88% from OPEC which currently is 15% (2.9 MBPD out of total consumption of 19.035 MBPD). Even today USA remains the largest consumer with largely regional production (N America) catering to its demand. If we see regional demand-supply mapping, the Americas are nearly balanced leaving the rest of the world to consume OPEC production. This leads to 5-6 countries (China, Japan, India, S Korea & Singapore) requirement balancing with OPEC surplus. The Americas is creating a regional Moat and forcing OPEC to focus on Asian consumption which is altering the bargaining power of the buyers. This is evident from the statement of the Indian Petroleum Minister that "oil producers should stop charging premium from its Asian buyers and offer better trade terms like selling oil without payment guarantee and on extended credit period":

3. Changing feed stock preference:

Natural gas has grown to become an alternative for transportation, power generation and industrial applications displacing crude demand. This has resulted in doubling of global natural gas demand from 1980 to 2010. From an environmental point of view, natural gas is a cleaner fuel than coal & crude adding traction to its demand. Lastly, natural gas is a regional play as there is limited role played by inter-continental movements. In short the markets have changed.4. Power of the alternative:

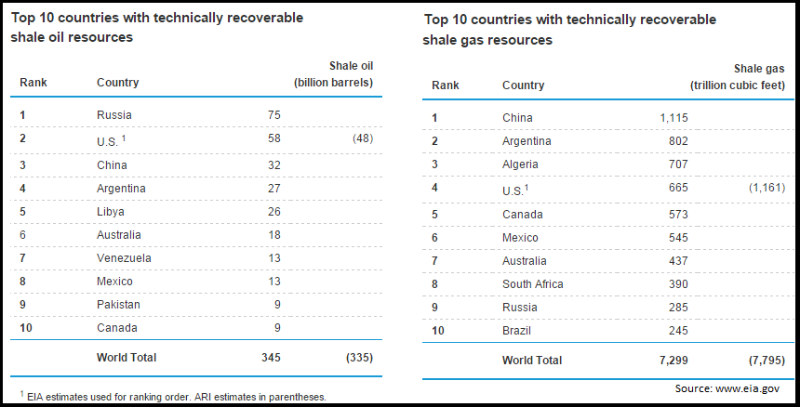

US shale is considered the main competitor to OPEC. Shale industry is a private initiative unlike OPEC which is NOC. Private initiative coupled with innovation has brought about this revolution that even at $ 45/bbl (WTI) production is not falling of the cliff indicating a powerful signal to unravel. Producers are trimming cost & changing the drilling patterns to ensure that even at these low prices production continues. Efforts are underway to propagate the shale technologies regionally to countries like Mexico. In order to balance the grade requirements, swaps are being planned which will further reduce dependence. Also, globally for energy security considerations, propagation of this technology is underway. China, OPEC's largest consumer and also one of the largest technical proven reserve holder of shale, is working to exploit its reserves.There is a Chinese Government grant to encourage shale production. Europe which has been dependent on Russia for its gas and had had supply disruption issues, is already prospecting for shale in the UK, Poland, Germany, Romania, Denmark and Hungary and commercial drilling is expected to commence this year. Countries like Britain are changing rules to fast track this progress. As a pattern, decoupling from the Middle East & localizing is visible:

5. The SWITCH:

The shift of the swing producer status from Saudi Arabia to US creates a switch mechanism on supplies as a result of which a ceiling on crude prices has emerged. Every time the prices fall below the marginal cost of production, supplies get switched off and once the prices move above supplies get switched on. This is facilitated by shale, Tar sands, etc being onshore business which can support this mechanics. As a result, quotas can only move the needle from the margin negative to marginal cost of shale.In summary:

Post the oil shock, surges in oil prices have been favorable to OPEC populations at the expense of the billions of consumers across the globe. Additionally, the middle east with a history of local issues, has always been perceived as an unstable source and engaged with due to lack of options. While coordinated action like quotas tends to work on short to medium terms to distort markets, in the long term competition happens at the level of competencies.Two quotes from Saudi Sheik Ahmed Zaki Yamani who was also a minister in OPEC for 25 years reflect the current developments very aptly:

"The stone age didn't end for lack of stones, and the oil world will end long before the end of oil".

"Technology is the real enemy".This shift in the industry dynamics makes is very interesting for top Asian buyers like China, Japan, India, Korea and Singapore to coordinate and unify the petroleum policies of its Countries and ensure the stabilization of oil markets in order to secure an efficient, economic and regular supply of petroleum to consumers free of distortion.

About M. S. Sriganesh:

Sriganesh tracks and analyzes markets from the perspective of its structure, competitiveness and evolution mainly using proprietary models derived from value chain analysis. These markets models used are capable of interpreting market dynamics for strategy formulation as well as price forecasting. Though these models are fungible across any market, specific use has been done in interested markets of crude, palm oil and metals.He can be reached through his Linkedin Page or Via email at mssganesh@gmail.com .

Source: Linkedin Article

Why OPEC Quotas Wont Work? http://t.co/MUNUgP7xDO pic.twitter.com/3DTJgFf8uw

— samuelR (@RajveerRawlin) September 22, 2015

Subscribe to:

Posts (Atom)

Market Insight

-

-

BAE Systems (OTCMKTS:BAESF) Stock Price Crosses Above Two Hundred Day Moving Average of $14.68 - Shares of BAE Systems plc (OTCMKTS:BAESF – Get Free Report) passed above its 200-day moving average during trading on Thursday . The stock has a 200-day mo...29 minutes ago

-

AI’s Impact In Medicine Around Development, Deployment, And Use - how can we make sure that we implement AI in a responsible way that provides mostly positive benefits while minimizing the potential downsides?1 hour ago

-

Cathie Wood Sees Value In Tesla Wreckage As Ark Buys $13M Worth Of EV Giant's Stock, Loads Up On Bitcoin And Ethereum ETFs - As *Tesla, Inc.* (NASDAQ:TSLA) fell for a fifth straight session on Thursday, breaching a significant psychologica read more2 hours ago

-

Homelessness Epidemic: the Public Sector is a Welfare Program - California’s homeless crisis proves the public sector is a welfare program and political tool. The California State Auditor released a report this month ...4 hours ago

-

U.S. Cities Fall Into A “Doom Loop” As The CRE Crisis Absolutely Explodes - In the entire history of the United States, we have never witnessed an urban collapse of this magnitude. During the pandemic, millions of Americans star...9 hours ago

-

Total Number of Stocks Is Shrinking - [image: total number of nyse nasdaq issues traded] The major averages may still be trending higher, but the total numbers of issues traded on the NYSE an...10 hours ago

-

Three Stocks: Taiwan Semiconductor, Meta, and UnitedHealth - Three Stocks: Taiwan Semiconductor, Meta, and UnitedHealth Taiwan Semiconductor Shares of the largest semiconductor chip manufacturer in the world traded 5...12 hours ago

-

S&P 500 PE Ratio - *Current S&P 500 PE Ratio:* 27.20 -0.06 (-0.22%) 4:00 PM EDT, Thu Apr 1812 hours ago

-

S&P 500 Yearly & Quarterly Pivot Levels | April - June 2024 - Ending the first week of January 2024 the S&P 500 had breached the Yearly Mid (R)esistance Level 1 (YMR1) at 4,781 to the upside. March consolidated above ...

13 hours ago

13 hours ago -

Thursday links: sharing your best work - Strategy - Passive investors don't change relative prices. (bloomberg.com) - A good outcome doesn't necessarily mean it was a good decision. (n...15 hours ago

-

Tracking inflation with sugar and sweets? - Inflation reflects how prices of goods and services in the economy are changing. One measure of inflation is the consumer price index (CPI), which is the c...19 hours ago

-

Daily Market Brief - Subscriber content. To subscribe to the Daily Market Brief please visit Market Services on NorthmanTrader.com. The Daily Market Brief is an in-depth market...22 hours ago

-

How Investors Can Seize Opportunities in NVDA Amid Market Volatility - According to Todd Gordon, the founder of Inside Edge Capital, NVIDIA Corporation (NVDA) is a strong buy despite a recent pullback. The chart analyst also s...22 hours ago

-

Bank Stocks Earnings Guide: Find “Bullish” Buys Today - Bank stocks are kicking off a busy earnings season. Here's what Green Zone Power Ratings says about one of the most popular bank ETFs. The post Bank Stoc...

22 hours ago

22 hours ago -

Debt Rattle April 18 2024 - John French Sloan A Woman’s Work 1912 • Prosecutors, Judges, Media Interfering in the November Election (PCR) • Iran’s ‘New Equation’ Reaches Way Beyon...23 hours ago

-

The Spear in AI's Back - *That real harm will result from the use of AI tools is a given. * *AI is like the powerful character in an action movie who looks invincible until they t...1 day ago

-

At the Money: Closet Indexing - At The Money: Andrew Slimmon on Closet Indexing (April 17, 2024) Are your expensive active mutual funds and ETFs actually active? Or, as is too of...1 day ago

-

Financial Nihilism Is A Symptom Of Society Gone Sick (You Need To Know This Concept) - I am not a financial nihilist and I reject those that advocate for it, because it goes totally against sound money management principles that use conservat...2 days ago

-

Shifting Wind - Weekly report covering Gold, Equities, Crude, Dollar. A look at trade opportunities and covering the model portfolio. The post Shifting Wind appeared fir...4 days ago

-

-

Unveiling the Golden Opportunity: Maximizing Profits with GLD - Are you ready to seize the golden opportunity in trading? In our last analysis, we forecasted a monumental breakout in the gold market, and the results h...1 week ago

-

Get More Out of Your Trades: Dukascopy Bank SA Cuts Withdrawal Fees - Dukascopy Bank SA would like to announce the reduction of withdrawal transfer fees on trading products, as follows: *Old fees* *New reduced fees* 3.5 EUR...2 weeks ago

-

Weekend Update - Trendline rejection (3/8/24) - SPX was rejected by the blue trendline Friday. The trendline had been sucessfully tested four times and held since November, until now. SPX has unable ...

5 weeks ago

5 weeks ago -

Catastrophic Risk: Investing and Business Implications - In the context of valuing companies, and sharing those valuations, I do get suggestions from readers on companies that I should value next. While I d...

2 months ago

2 months ago -

Hello world! - Welcome to WordPress. This is your first post. Edit or delete it, then start writing!2 months ago

-

Teaching Johns Hopkins A Privilege Lesson - by Not Sure01/12/24Johns Hopkins Hospital Chief Diversity Officer Sherita Hill Golden sent a letter out essentially implying that all people who don’t look...3 months ago

-

Mungerisms: Timeless Wisdom from Charlie Munger on Life and Business - "Mungerisms" are succinct expressions of wisdom and insights coined by Charlie Munger, the Vice Chairman of Berkshire Hathaway and Warren Buffett's longtim...4 months ago

-

If You Find Deer or Elk Antlers on the Ground, Leave Them There, Say Some States - Even though elk do shed their antlers naturally, collecting them brings up a number of ethical issues.6 months ago

-

It’s Crunch Time for The Daily Doom and Doom Time for The Great Recession Blog - The Great Recession Blog is officially done for good, and it remains to be seen if all my writing continues on TheDailyDoom.com. If my writing on economi...9 months ago

-

Innovative Industrial Properties Stock a Great Way to Play Pot Sector - *IIPR Stock Represents a Long-Term Opportunity* Marijuana stocks briefly attracted investors' attention following the 2022 mid-term elections, when Maryl...1 year ago

-

2008 analogue - The 2008 analogue tape looks very interesting from where we stand. Let's anchor it to the next two Fed meetings -- since that's all that matters -- and i...

1 year ago

1 year ago -

Back to trade with Bar Replay - It is often said that one should not be sad about the past, but sometimes it can be nice to return to it. Who would like to buy Tesla for $1 and experience...1 year ago

-

After This Holiday Rally, You Better Know When To Walk Away - This week’s investor insight will make you think twice about the current stock and bond rally as we head into the end of the year. We get a lot of questi...1 year ago

-

How Africa Can Escape Chronic Food Insecurity Amid Climate Change - The toll of extreme weather events on crops underscores the region’s challenges and need for policies to save lives and protect livelihoods.1 year ago

-

12 Bear Market Rules To Live By – Survive & Thrive In The Next Bear Market - 12 Bear Market Rules To Live By – Survive & Thrive In The Next Bear Market [image: Bear Market Rules Survival Guide] I grew up in the 1970s-1980s when th...1 year ago

-

Growth Companies – Getting What You Want - What do the growth companies in your field have in common? How are they doing so well and what can you learn from them? Growth companies usually make a pro...1 year ago

-

-

Blog Post Title - What goes into a blog post? Helpful, industry-specific content that: 1) gives readers a useful takeaway, and 2) shows you’re an industry expert. Use your c...2 years ago

-

Foot Locker Crushed Q2 Earnings Expectations Sending Stock Higher - Plus, AstraZeneca said its antibody therapy reduced the risk of developing COVID-19 symptoms by 77%, The Topps Co’s SPAC merger is off, and Elon Musk annou...2 years ago

-

Elliott Wave Stock Market Update - July 10th - The market has continued its rally to higher highs and it doesn't seem like it wants to stop. We now have a new ATH at 4371 which are NASDAQ levels s...

2 years ago

2 years ago -

The Psychology of QE is Far More Important Than the Amount of It - Let's discuss what QE really does vs the psychology of QE.2 years ago

-

Hello world! - Welcome to WordPress. This is your first post. Edit or delete it, then start writing!3 years ago

-

Trading: Opportunities Are Dispersed - Opportunities are dispersed. You might have an... *READ THE REST OF THE ARTICLE ON THE NEW WEBSITE: JIM ROGERS TALKS MARKETS * *Jim Rogers is a legendary i...

3 years ago

3 years ago -

Market Signals for the US stock market S and P 500 Index and Indian Stock Market Nifty Index for the Week beginning November 09 - Indicator Weekly Level / Change Implication for S & P 500 Implication for Nifty* S & P 500 3509, 7.32% Bullish Bullish Nifty 12264, 5.34% Neutral ** Bullis...3 years ago

-

November report "Is it True, as David Hume (1711 – 1776) postulated that, "Nothing is esteemed a more certain sign of the flourishing conditions of any nation than the lowness of interest"?" published. https://bit.ly/2y4LJZQ - November report "Is it True, as David Hume (1711 – 1776) postulated that, "Nothing is esteemed a more certain sign of the flourishing conditions of any n...3 years ago

-

Fully Automated Trend Trading w/ Stocks Or Options - There’s a lot of research to support the usage of trend indicators as simple risk reduction elements that can be layered onto an existing strategy. Howev...3 years ago

-

2020 Top Investment Picks – Q3 Update - At the beginning of the year, I put together a list of Top Investment Picks for 2020 from the investment community and track them on this website. This is ...3 years ago

-

Upside-Down Markets: Profits, Inflation and Equity Valuation in Fiscal Policy Regimes - I just published a new long-form piece through OSAM entitled “Upside-Down Markets: Profits, Inflation and Equity Valuation in Fiscal Policy Regimes.” In th...3 years ago

-

The last of 12326 - February 22nd 2012..... First post... https://permabeardoomster.blogspot.com/2012/02/can-anyone-fly-plane.html -- This post will be the last under the o...

3 years ago

3 years ago -

-

Ultramarathoner Runs Over 200 Miles in Backyard, Wins Golden Toilet Paper Roll - Strange times indeed. In the land “BC,” before coronavirus, people ran long distances in foot races, and toilet paper wasn’t coveted. Things have changed. ...4 years ago

-

One Year Later - A year ago today I lost my father and my best friend, everyone here lost their mentor and a friend. Dad and I spent the last 7 years of his life living tog...4 years ago

-

-

Advanced Micro Devices (AMD) Retreating Towards Key Support Around $25.60-$27 -

AMD has failed to clear the 2018 high around $34.20. It is retreating, and has broken an August/September sup...

4 years ago -

Advanced Search is Now on Stocktwits - Advanced Search Is Now on Stocktwits Come rain or shine, the Stocktwits community shares over 200,000 messages per day. That includes charts, news, trade i...4 years ago

-

Nightly Algo Report – December 6, 2018 - To access this post, you must purchase Premium Plan or Premium Plan - Annual. The post Nightly Algo Report – December 6, 2018 appeared first on Elliottwa...5 years ago

-

Don’t be Fooled by the Pullback in the Dollar Because…. - Don’t be fooled by the pullback in the U.S. dollar today because the greenback could still strengthen further before the end of the year. Nearly all of the...5 years ago

-

A look at the bull market ahead - My latest missive on the near-term stock market outlook can be seen at Financial Sense web site. You can see it by clicking on the following link: https:/...6 years ago

-

Weekly Videos - This week’s video will be posted on the new home for Short Takes. If all goes well, it will appear sometime between 6:00 and 8:00 pm ET.6 years ago

-

Gold Miners near a buy zone - Gold cleared a several month long consolidation a few weeks ago as it cleared $1300, and has since been consolidating as it drifts back to […] The post G...6 years ago

-

Current Account Deficits and Safe Assets - The International Monetary Fund has issued its External Sector Report for 2017, and among its key findings: “Global current account imbalances were broadly...6 years ago

-

Kafka For The Twenty First Century - I've been spending a slightly frustrating day trying to update my payment details at google. To log in to my admin console I need to log in using my G Sui...

7 years ago

7 years ago -

Gold Unleashed by Fed - Gold's next major upleg was likely unleashed by a very-dovish FOMC this week, which now has its hands tied on hiking rates or being hawkish due to the US e...7 years ago

-

August 24th Blogger Sentiment Poll - There are more bulls than bears in this week's poll. Blogger Sentiment Poll Participants: 24/7 Wall St (N) Carl Futia (+) Dash of Insight (+) Elliot Wave L...14 years ago

Forex Insight

-

Greece Current Account (YoY) down to €-3.161B in February from previous €1.703B - Read more on https://www.fxstreet.com31 minutes ago

-

Chart Art: Can Risk Aversion Drag EUR/JPY to Its Range Support? - News of escalating military conflict between Israel and Iran pushed safe havens like the yen higher. Will this drag EUR/JPY to a support zone?4 hours ago

-

British Pound Trade Setups & Technical Analysis: GBP/USD, EUR/GBP, GBP/JPY - This article offers a comprehensive examination of GBP/USD, EUR/GBP, and GBP/JPY from a technical perspective, analyzing chartist formations and market sen...9 hours ago

-

GBP/USD eyes retail sales - The British pound is having a quiet week and that trend has continued on Thursday . In the North American session, GBP/USD is trading at 1.2450, down 0.04%...16 hours ago

-

Don’t be Fooled by the Pullback in the Dollar Because…. - Don’t be fooled by the pullback in the U.S. dollar today because the greenback could still strengthen further before the end of the year. Nearly all of the...5 years ago

-

EUR/USD Weekly Outlook - EUR/USD's decline attempt was contained at 1.0494, above 1.0493 support and rebounded. Initial bias stays neutral this week first. On the upside, break of ...7 years ago

-

Loonie and Aussie Share Downward Bond - In yesterday’s post (Tide is Turning for the Aussie), I explained how a prevailing sense of uncertainty in the markets has manifested itself in the form of...12 years ago

India Market Insight

-

Mid-day Mood | Market trades in red as Middle-East crisis deepens, volatility jumps 4% - [image: Mid-day Mood | Market trades in red as Middle-East crisis deepens, volatility jumps 4%] Broader indices underperformed benchmark indices on April 1...1 hour ago

-

Sun Ingress and Israeli Airstrikes In Iraq : Bank Nifty 19 April 2024 Trade Plan - Foreign Institutional Investors (FIIs) exhibited a Bearish stance in the Bank Nifty Index Futures market by Shorting 21847 contracts with a total value o...4 hours ago

-

Rupee falls 29 paise to close at 82.68 against US dollar - During the day, the rupee touched a high of 82.45 and a low of 82.68 against the greenback. On Friday, the rupee had settled at 82.39 against the dollar.

10 months ago

10 months ago -

-

ES Hourly cloud and 4 Hour chart - - ES Hour moving towards the hourly cloud which may act as resistance. - 4 Hour chart shows a possible bullish candle which may give new high's ...

2 years ago

2 years ago -

JUST NIFTY BLOG 10-01-2020 - Bulk Deals FII DII Stats Date # of Deals Total Volume (In Millions) 01-01-1970 0 0.00 Click here to see all Bulk Deals Date Category Buy Amount (Rs. Cror...4 years ago

-

Vist Note on Federal Bank - We recently met the senior management of Federal Bank which is one of the old private sector banks with a distribution network of 1252 branches (48% Kerala...6 years ago

-

Nifty Bulls bounces ferociously holding 9930,EOD Analysis - FII's bought 4.8 K contract of Index Future worth 262 cores ,9.7 K Long contract were added by FII's and 4.8 K Short contracts were added by FII's. Net Ope...6 years ago

-

Midcap & Smallcap Index Corrects, Lets Come Back To Fundamentals Again - Midcap Index had made a high of 18511 on 16th May 2017, fell almost 7% and is currently trading at 17230. Smallcap Index made all time high of 7679 on 11th...6 years ago

-

Market outlook for 30/10/2016 - *Nifty closed up 22.75 points (0.26%) at 8638.00* while Future closed at 8667.40, premium of 29.40 points. *Bank Nifty closed up 41.35 points (0.21%) at 19...

7 years ago

7 years ago -

Option Open Interest for 28-10-2016 - Inference The index opened flat to positive and after making an initial low around 8581 saw some short covering to close at 8638.00, gain of 22.75 points. ...

7 years ago

7 years ago -

Market Review for 23rd August 2016 - *Nifty (8629)* we said ‘technically trend is still intact but there exists selling pressure near 8746 and support around 8600 zones’ the Nifty unfolded as...7 years ago

-

ITC To Resume Cigarette Manufacturing - ITC manufactures a range of cigarette brands, including India Kings, Classic, Gold Flake, Navy Cut, Capstan, Bristol, Flake, Silk Cut, which are manufactur...8 years ago

-